How COVID-19 Has Impacted Life Insurance in 2024

How COVID-19 Has Impacted Life Insurance in 2024

The COVID-19 pandemic has had far-reaching effects on virtually every sector, and life insurance is no exception. As we navigate through 2024, it becomes increasingly clear that the pandemic has reshaped the landscape of life insurance in profound ways. From shifting consumer attitudes to evolving policy structures, the ripple effects of COVID-19 continue to influence the industry. This article explores how COVID-19 has impacted life insurance in 2024, examining changes in consumer behavior, policy trends, technological advancements, and regulatory shifts.

1. Shifting Consumer Attitudes and Behavior

The pandemic has dramatically altered the way people think about their health, finances, and future security. Prior to COVID-19, life insurance was often considered a low-priority financial product for many individuals. However, the widespread health crisis and its accompanying uncertainty have pushed life insurance to the forefront of financial planning for many.

1.1 Increased Awareness and Demand

In 2024, there is a noticeable increase in consumer awareness regarding the importance of life insurance. The pandemic has heightened the understanding of the need for financial protection in the face of unexpected events. Many individuals who previously overlooked life insurance are now actively seeking coverage to ensure that their loved ones are financially secure should something happen to them.

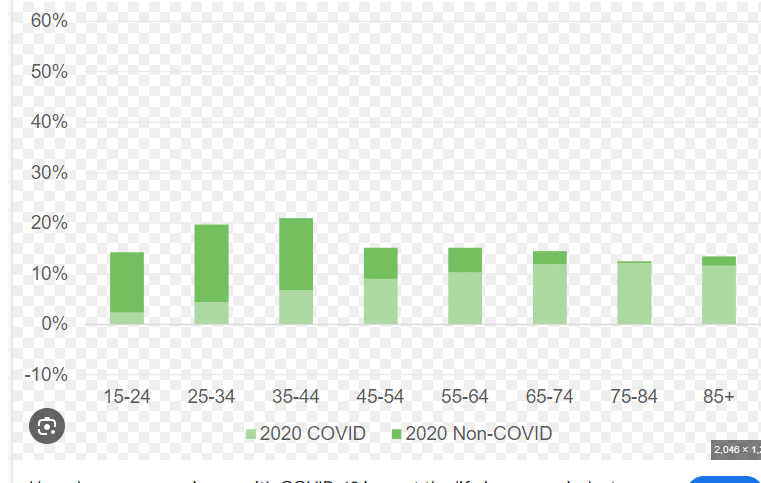

1.2 Shift in Demographics

The demographic profile of life insurance policyholders has also shifted. Younger generations, particularly Millennials and Gen Z, are increasingly recognizing the value of life insurance. The pandemic has catalyzed a shift in attitudes, with younger individuals acknowledging the importance of planning for the future and protecting their families. This demographic shift is prompting insurers to tailor their products and marketing strategies to appeal to a younger audience.

2. Evolution of Policy Structures

The pandemic has prompted significant changes in the way life insurance policies are structured. Insurers have had to adapt to the new reality by revising their offerings and adjusting policy terms to address emerging needs and concerns.

2.1 Enhanced Coverage for Pandemic-Related Risks

In response to the pandemic, many insurers have introduced new policy features and riders specifically designed to address pandemic-related risks. Coverage for COVID-19-related illnesses and death has become a standard inclusion in many policies. Additionally, insurers are offering expanded coverage options for other health crises, acknowledging the increased demand for protection against a broader range of risks.

2.2 Flexibility and Customization

The pandemic has underscored the importance of flexibility and customization in life insurance policies. Many insurers have responded by offering more flexible policy terms, allowing policyholders to adjust coverage amounts, premiums, and beneficiaries as needed. This flexibility caters to the evolving financial situations of individuals and families, providing a more tailored approach to life insurance.

2.3 Digital Transformation of Policies

The shift toward digitalization has accelerated due to the pandemic. Insurers are increasingly offering digital platforms for policy management, claims processing, and customer service. This transformation not only enhances the convenience and efficiency of interactions but also aligns with the growing preference for online solutions among consumers.

3. Technological Advancements

The pandemic has acted as a catalyst for technological innovation within the life insurance industry. Insurers are leveraging technology to improve underwriting processes, enhance customer experiences, and streamline operations.

3.1 Remote Underwriting and Telemedicine

Remote underwriting and telemedicine have become integral components of the life insurance process in 2024. The pandemic has demonstrated the value of remote assessments and virtual consultations, allowing insurers to conduct medical underwriting and risk assessments without in-person visits. Telemedicine services are now commonly incorporated into life insurance policies, providing policyholders with access to virtual healthcare consultations and resources.

3.2 AI and Data Analytics

Artificial intelligence (AI) and data analytics are transforming the way insurers assess risk and personalize policies. AI-driven tools enable more accurate risk assessment and pricing, while data analytics help insurers identify emerging trends and customer preferences. The use of predictive analytics allows insurers to anticipate potential risks and tailor products to meet the evolving needs of policyholders.

3.3 Digital Customer Engagement

The shift toward digital customer engagement has accelerated as a result of the pandemic. Insurers are investing in user-friendly digital interfaces, mobile apps, and online customer service channels to enhance the overall customer experience. This digital transformation not only improves accessibility but also empowers policyholders with greater control over their insurance management.

4. Regulatory and Industry Changes

The impact of COVID-19 on life insurance extends beyond consumer behavior and policy structures to encompass regulatory and industry changes. Regulators and industry stakeholders have had to address new challenges and adapt to the evolving landscape.

4.1 Regulatory Adjustments

Regulators have introduced various measures to address the challenges posed by the pandemic. These adjustments include temporary relaxations of regulatory requirements, extended deadlines for policyholders, and guidelines for insurers to manage pandemic-related risks. Regulatory bodies are closely monitoring the industry’s response to the pandemic and making adjustments as needed to ensure consumer protection and industry stability.

4.2 Industry Collaboration and Support

The pandemic has highlighted the importance of industry collaboration and support. Insurers, industry associations, and government agencies have worked together to provide guidance and support to policyholders and businesses. Initiatives such as financial assistance programs, educational resources, and industry forums have played a crucial role in navigating the challenges brought about by the pandemic.

4.3 Focus on Mental Health and Well-being

The pandemic has brought increased attention to mental health and well-being, and the life insurance industry is responding accordingly. Insurers are incorporating mental health support into their policies and offering resources for policyholders to address mental health concerns. This holistic approach recognizes the impact of mental well-being on overall health and financial security.

5. Looking Ahead: Future Trends and Considerations

As we move further into 2024, the life insurance industry will continue to evolve in response to the ongoing impact of COVID-19. Several key trends and considerations are likely to shape the future of life insurance.

5.1 Continued Emphasis on Health and Wellness

The pandemic has underscored the importance of health and wellness, and this emphasis is expected to persist. Insurers are likely to continue incorporating health and wellness features into their policies, such as incentives for healthy behaviors, access to wellness programs, and coverage for preventive care. The focus on holistic health will be a central theme in the evolution of life insurance products.

5.2 Integration of Emerging Technologies

Emerging technologies, such as blockchain and advanced analytics, are poised to play a significant role in the future of life insurance. Blockchain technology has the potential to enhance transparency and security in policy management and claims processing. Advanced analytics will continue to drive innovation in risk assessment and product customization, allowing insurers to offer more personalized solutions.

5.3 Greater Emphasis on Financial Planning

The pandemic has highlighted the importance of comprehensive financial planning, and life insurance will play a crucial role in this regard. Insurers are expected to collaborate with financial advisors and planners to offer integrated solutions that address broader financial needs, including retirement planning, estate planning, and legacy planning.

5.4 Evolving Consumer Expectations

Consumer expectations are evolving, and insurers will need to adapt to meet these changing demands. Transparency, convenience, and personalized service will be key factors in attracting and retaining policyholders. Insurers that can effectively leverage technology to provide seamless and personalized experiences will be well-positioned for success in the post-pandemic era.

Conclusion

COVID-19 has left an indelible mark on the life insurance industry, reshaping consumer attitudes, policy structures, and technological advancements. As we move through 2024, the industry continues to adapt and evolve in response to the ongoing impact of the pandemic. Increased awareness of the importance of life insurance, advancements in technology, and shifts in regulatory frameworks are all contributing to a dynamic and evolving landscape. The lessons learned from the pandemic are likely to drive further innovation and transformation within the industry, ultimately leading to more resilient and responsive life insurance solutions for the future.

Leave a Reply